Most vehicle damage disputes in auto transport don't happen because carriers are negligent; they happen because shippers assume they were covered when they weren't.

Car shipping insurance does not cover everything that can go wrong during transport. Standard auto transport insurance excludes personal belongings, weather events, pre-existing damage, and mechanical issues, and most shippers only discover these gaps after a claim is denied. Knowing what's excluded before you book is the most effective way to protect your vehicle and your money.

Safeeds Transport works exclusively with FMCSA-licensed, insured carriers. Before you ship, get a free quote and ask our team exactly what coverage applies to your shipment.

What Does Car Shipping Insurance Actually Cover?

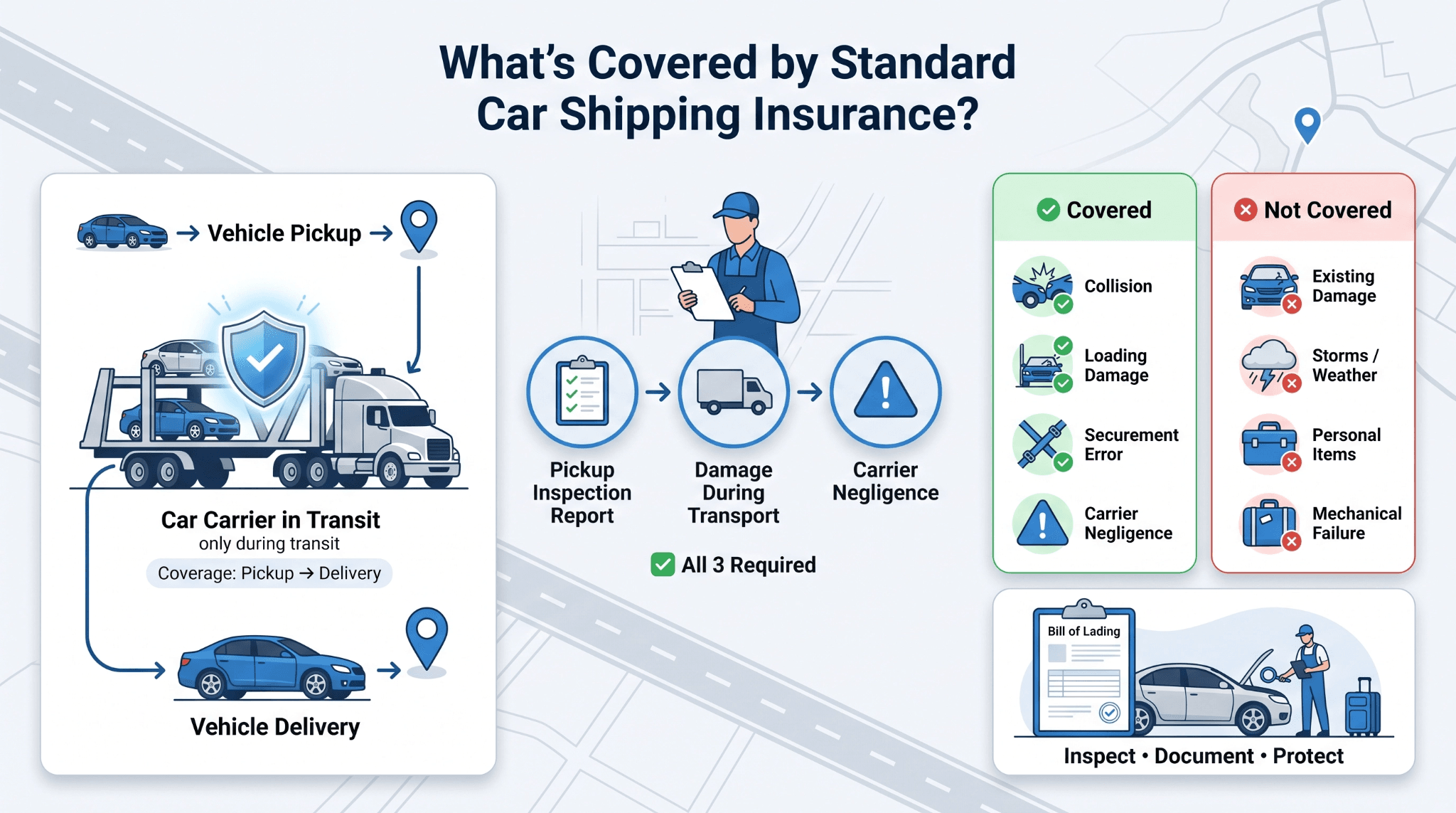

Standard auto transport insurance is a cargo liability policy held by the carrier. It covers specific damage under specific conditions, not everything that could go wrong in transit.

What is cargo liability coverage in auto transport?

Under FMCSA regulations, all licensed carriers must maintain cargo liability insurance. This covers physical damage caused directly by carrier negligence, improper securing, loading errors, or a driver-caused accident.

For a claim to be valid, three conditions must be met. Understanding these upfront prevents surprises when a dispute arises after delivery.

Damage occurred while the vehicle was in the carrier's possession

Damage was not present at pickup, as documented on the inspection report

Damage resulted from carrier negligence, not an external event

Is my car insured during shipping from the moment it's picked up?

Yes, within limits. Coverage begins when the carrier takes possession at pickup and ends at delivery. The Bill of Lading, signed by both parties at pickup, is the official condition record. Damage that cannot be traced to that document is nearly impossible to claim.

The table below summarizes what standard cargo liability does and does not cover, so you know exactly where the protection starts and stops before your vehicle is loaded.

Coverage Trigger | Covered |

Carrier negligence (loading error, accident) | Yes |

Pre-existing damage at pickup | No |

Weather events during transit | No |

Personal items inside the vehicle | No |

Mechanical or electrical failure | No |

What Car Shipping Insurance Won't Cover: The Real Exclusions

This is where most disputes originate. Cargo liability covers carrier negligence and nothing else. These exclusions are not fine print; they are structural features of how auto transport insurance works.

Does car shipping insurance cover personal items left inside the vehicle?

No. Cargo liability applies to the vehicle only, not to personal property inside it. GPS units, laptops, clothing, and bags are not covered under any standard transport policy. Carriers often prohibit personal items in their terms of service, and in all cases, the shipper bears full responsibility for anything left inside the car.

There are two practical steps every shipper should take before pickup to avoid this loss entirely. Both are simple and take only a few minutes to complete.

Remove all personal items from the vehicle before the driver arrives

If removal is not possible, photograph everything and understand that no recovery will come through a transport insurance claim

Are weather and natural disaster damages covered during transport?

No. Hailstorms, flooding, fallen debris, and high winds are excluded from standard cargo liability. These events fall outside carrier control and do not meet the negligence threshold required to trigger a valid claim.

A common misconception is that enclosed transport changes this. It does not. Enclosed transport reduces physical exposure to the elements, but the underlying insurance policy carries the same weather exclusions as open transport. The protection is physical, not financial.

What happens if pre-existing damage gets disputed after delivery?

This is the most frequently contested scenario in auto transport claims. If a scratch or dent existed before pickup, it cannot form the basis of a claim, even if the shipper did not notice it until delivery. Carriers reference the pickup inspection report to demonstrate pre-existing damage, and if that report was signed without a thorough review, the carrier's documentation becomes the controlling record.

Shippers transporting a car without insurance documentation in order to face the same risk, no paper trail means no viable dispute. The condition report completed at pickup is not a formality. It is your primary legal protection and the single document that determines whether a post-delivery claim can succeed.

Does auto transport insurance cover mechanical or electrical problems?

No. Cargo liability is not a mechanical warranty. A dead battery, sensor fault, or transmission issue that was not documented before shipping is not covered, regardless of when it appeared during or after transit. The only exception is a documented physical impact that caused visible, verifiable mechanical damage directly attributable to carrier negligence.

The table below brings all four exclusion categories together in one place, showing why each applies and what shippers can do to manage the risk before booking.

Exclusion | Why It's Excluded | What to Do |

Personal items | Coverage is vehicle-only | Remove all items before pickup |

Weather/acts of God | Outside carrier control | Consider enclosing high-value vehicles |

Pre-existing damage | Not caused during transit | Document all damage thoroughly at pickup |

Mechanical issues | Not a physical cargo loss | Test and photograph the vehicle before shipping |

Damage below deductible | Policy minimums may apply | Request full policy details before booking |

How Does Carrier vs. Broker Insurance Work and Why Does It Matter?

Many shippers book through a broker and assume the broker insures their vehicle. That assumption is incorrect, and it creates real complications when a claim needs to be filed at the other end of the shipment.

What insurance does a car shipping broker actually carry?

Brokers and carriers carry fundamentally different types of insurance, and understanding that difference before booking can save significant time and frustration if a claim ever needs to be filed. Here is what a broker's insurance coverage actually includes and where it stops.

Brokers are required to carry a surety bond of at least $75,000 under FMCSA rules

They may also carry contingent cargo insurance, but this only activates when the carrier's policy fails to respond or is found insufficient

Contingent coverage is difficult to trigger and rarely provides the protection shippers expect

A broker's general liability policy does not cover physical damage to your vehicle during transit under any circumstances

Who is responsible for the damage, the broker or the carrier?

The line of responsibility between brokers and carriers is one of the most misunderstood areas in auto transport, and it matters most at the moment a claim needs to be filed. The breakdown below clarifies exactly where each party stands.

The carrier is the legally responsible party for all cargo damage during transit

The broker facilitates the shipment and can advocate during a claim, but has no legal obligation to compensate the shipper from their own funds

The only exception is if negligence in carrier selection by the broker can be demonstrated

Requesting a Certificate of Insurance from the assigned carrier before pickup is a non-negotiable step, not an optional one

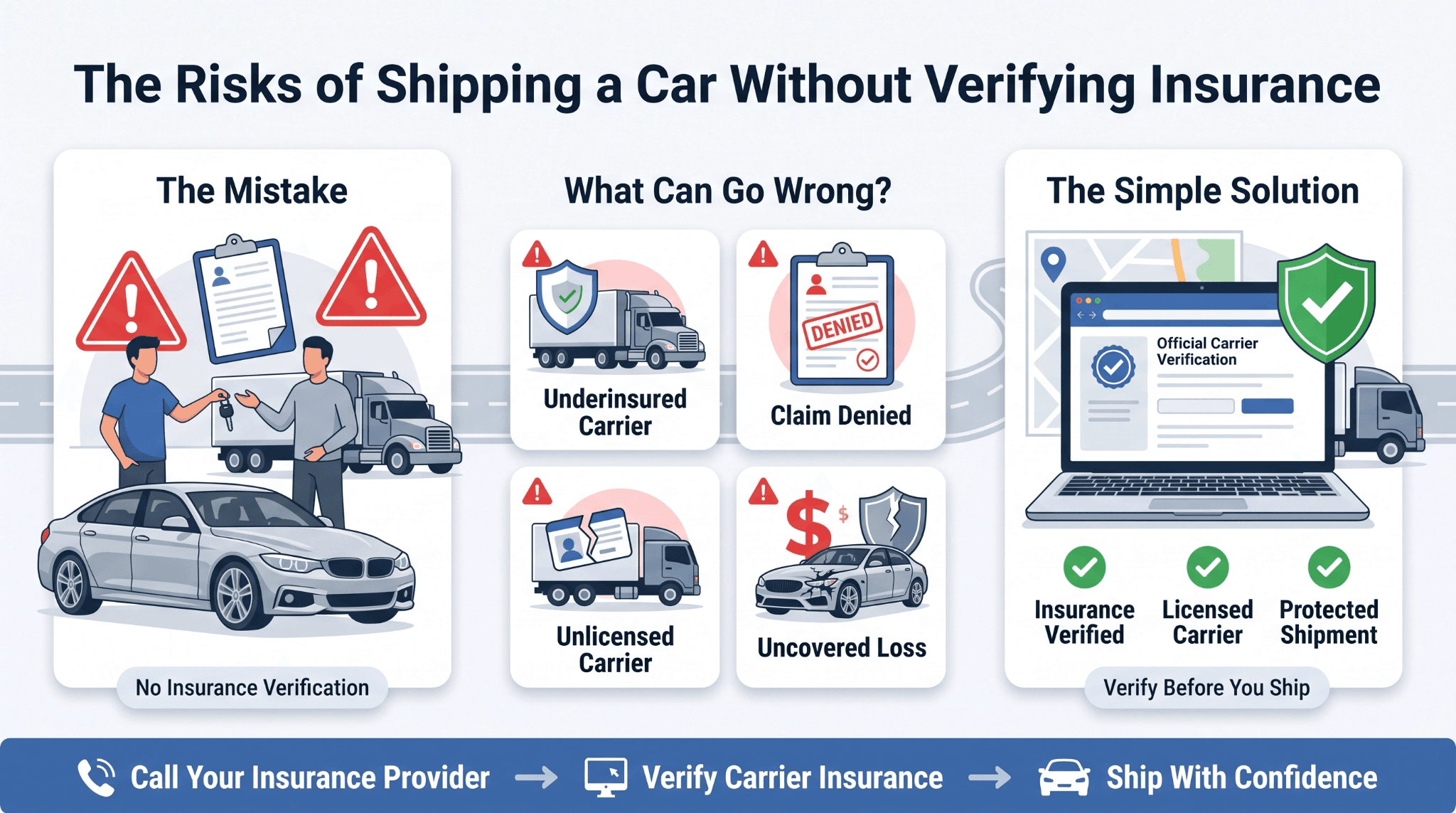

What Happens When You're Transporting a Car Without Adequate Insurance?

Transporting a car without verifying coverage is one of the most avoidable and costly mistakes in auto transport. The scenarios below are not edge cases; they are documented patterns that repeat across the industry every year.

Does personal auto insurance cover a car during transport?

In most cases, no. Standard personal auto policies cover vehicles while being driven, not while loaded on a transport carrier. Some policies include theft coverage that may extend to transit, but in-transit collision and cargo damage are typically excluded.

Before shipping, call your insurer and ask one direct question: Does my policy cover physical damage while a third-party carrier is transporting my vehicle? Do not interpret general policy language as confirmation; get the answer in writing before your vehicle is picked up.

What are the risks of transporting a car without verifying insurance?

Skipping insurance verification before booking creates a range of serious financial risks. Each of the scenarios below has played out in real transport disputes, and all of them are avoidable with a single verification step before the shipment is confirmed.

The carrier may be underinsured, with policy limits too low to cover your vehicle's actual value

A claim may be denied because the damage falls under an exclusion that was never disclosed

The carrier may be unlicensed and uninsured entirely, leaving no legal recourse for the shipper

Damage that exceeds policy limits leaves the shipper with no recovery path, regardless of fault

The FMCSA's carrier lookup tool allows shippers to verify a carrier's operating authority and insurance status before any vehicle changes hands. It takes under two minutes and eliminates the highest-risk scenarios in transporting a car without verified coverage.

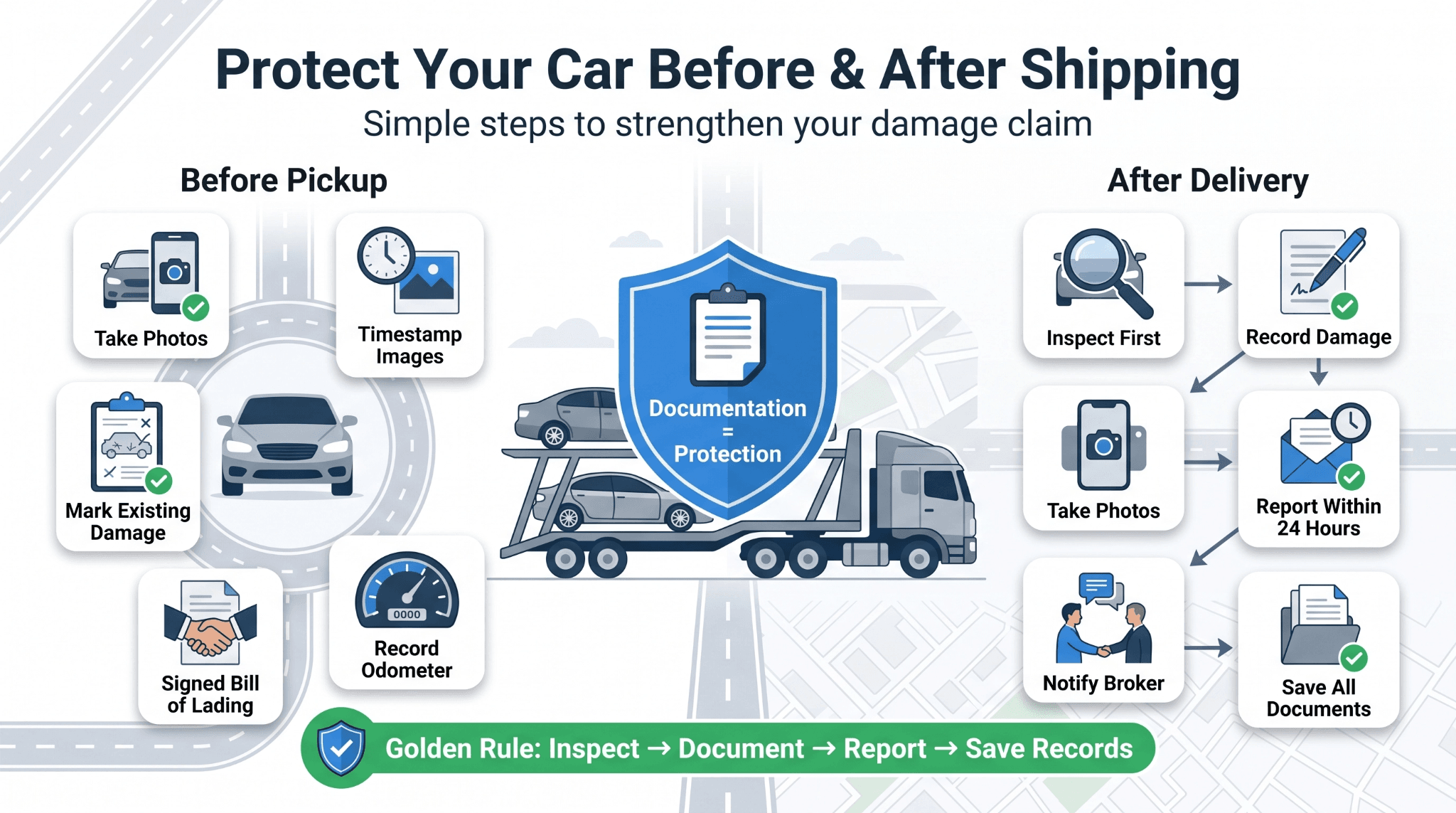

How Do You Protect Yourself Before and After Shipping?

Documentation is the single most effective protection against a denied claim, regardless of which carrier handles the shipment or which broker the booking was placed through. The steps below apply to every shipment, every vehicle type, and every route.

What should you document before your car is picked up?

A thorough pre-shipping record gives you a legally defensible baseline if a dispute arises after delivery. The following five steps should be completed before the driver arrives, without exception.

Photograph the vehicle from all angles: front, rear, both sides, roof, and all four corners

Use timestamped photos; device timestamps create a defensible, verifiable record

Note every existing scratch or dent on the Bill of Lading; do not sign a clean report on a vehicle with pre-existing damage

Confirm that the driver signs the condition report, and both parties should retain a physical copy

Record the odometer reading before the vehicle is loaded onto the carrier

What should you do if your car arrives with damage?

If damage is discovered at delivery, the order of actions is just as important as the actions themselves. Moving through these steps out of sequence, particularly signing before inspecting, can invalidate an otherwise legitimate claim.

Do not sign the delivery receipt until the vehicle has been fully and carefully inspected

Note all visible damage on the delivery report before signing anything

Photograph the damage immediately, with the driver present if possible

Contact the carrier in writing within 24 hours of delivery

Notify your broker, a reputable broker will begin advocating for resolution immediately

Preserve all documentation: the Bill of Lading, pickup photos, delivery photos, and all written correspondence

As consumer guidance from the FMCSA makes clear, shippers who fail to document damage at the time of delivery significantly reduce their ability to pursue a valid claim afterward.

What Shippers Ask About Car Shipping Insurance

Every shipper has questions about coverage before handing over their vehicle, and the answers are not always straightforward. The questions below address the most common gaps and concerns that come up after a quote is requested.

Does enclosed transport provide better insurance coverage than open transport?

Not automatically. Enclosed transport reduces physical exposure but carries the same policy exclusions as open transport. For broader financial coverage, ask about supplemental insurance options regardless of which transport type you choose.

Can I add supplemental insurance for a high-value vehicle?

Yes. Third-party insurers offer in-transit vehicle coverage that fills the gaps left by standard cargo liability. This is particularly relevant for classic, luxury, or modified vehicles whose market value may exceed a carrier's standard policy limits. Safeeds can connect you with supplemental coverage options based on your vehicle type and route.

What is a Certificate of Insurance and should I ask for one?

A Certificate of Insurance (COI) confirms a carrier's active coverage, policy limits, and coverage dates. Every legitimate carrier can provide one on request. Asking for a COI before pickup is one of the most effective steps in avoiding the risks of transporting a car without verified coverage in place.

How long do I have to file a damage claim after delivery?

Most cargo liability policies require written notice of damage within 9 months and a formal claim within 2 years, but individual carrier terms vary. The safest approach is written notice to the carrier within 24 hours of delivery and a formal claim submission within 30 days.

Does Safeeds verify carrier insurance before assigning a shipment?

Yes. Every carrier dispatched through Safeeds is verified for active FMCSA operating authority and current cargo insurance before assignment. Shippers can request the assigned carrier's COI at any time through our support team.

Ship With a Broker That Verifies Every Carrier Before You Book

Understanding car shipping insurance gaps is only half the equation. The other half is choosing a transport partner that does the verification work before your vehicle leaves your driveway.

Safeeds Transport works exclusively with FMCSA-licensed, insured carriers. Every carrier in our network is screened for active cargo coverage before assignment. Our team provides full transparency on coverage details, answers your insurance questions before you commit, and advocates on your behalf if anything goes wrong in transit. Get your free car shipping quote in 30 seconds, and ship knowing exactly what's covered.